| |

|

|

Latest events and updates about Account Aggregator ecosystem

|

|

|

|

|

88.63 million

Consent requests fulfilled

|

|

77.26 million

Accounts linked on AA

|

|

600 FIs

Actively engaged in AA adoption

|

|

507 FIs

Live on AA

|

|

155 FIPs

Live on AA

|

|

447 FIPs

Live on AA

|

|

87 FIPs

Available on 4 or more AAs

|

|

|

370 FIs

17 TSPs

Sahamati Certification Framework

|

|

185 Signatories

AA Participation Terms

|

|

1,619 UAT

711 Prod

Entries in AA Registry

|

|

44,818(cumulative)

Grievances handled

|

|

17,555(cumulative)

Grievances resolved

|

|

|

|

|

|

|

|

|

|

The Reserve Bank of India (RBI) released its Financial Stability Report for June 2024 a few weeks ago. A significant part of the report addresses emerging cyber and other risks that are looming in the financial sector. In the realm of cyber risks, the financial sector has experienced over 20,000 cyber intrusions and digital attacks in the past 20 years, leading to losses totaling $20 billion or 2000 Crores. Additionally, the amount of fraud reported across banks in FY24 increased by 300% from FY23 levels. The majority of these frauds were concentrated in digital payments and digital journeys.

On the lending side, the report highlights the rapid growth in the unsecured retail loan segment. This segment has experienced a 23% growth in the last two years compared to a 12-14% overall credit growth. The report also noted a significant chunk of frauds associated with loan portfolios compared to a much smaller number in cards and other internet frauds. In the consumer credit segment, delinquency levels among borrowers with personal loans under ₹50,000 remain elevated. NBFC-Fintech lenders, who hold the largest share in both sanctioned and outstanding amounts, exhibit the second highest delinquency levels, surpassed only by small finance banks. This increase in the amount of unsecured retail loan segment can pose a threat to the stability of the Indian financial sector, if left unchecked.

In a recent interaction, M Rajeshwar Rao, Deputy Governor, RBI mentioned the impairment framework prescribed under Indian Accounting Standards and said that while the framework was forward-looking, it had been observed that some non-banking financial companies primarily relied on the 30 days-past-dues (DPD) criterion for loan loss. Mr. Rao further stated that DPD, being a lagging indicator, is not always in sync with using the forward-looking approach of Expected Credit Loss (ECL). The statement reiterates the need for lenders to strengthen their capability in tracking lead indicators, which can warn banks and NBFCs of early stress signals in their portfolio, rather than just relying on lag indicators such as 30 DPD or bureau scores.

The AA framework, as a game changing framework, empowers banks and NBFCs to contain fraud at the time of loan processing by ensuring tamper-proof bank statements are available to lenders. A survey with leading banks highlighted that forged bank statements are estimated to account for 0.5-4% of the underwriting applications. The number has been reported to be as high as 10% for digital NBFCs. Authentic banking data also enables lenders to cross-validate the profile information and other signals received from bank statements with other documents such as Aadhaar, PAN Card and Bureau Reports.

Further, the recurring consent feature enables lenders to build robust early warning signals that can help them take corrective actions on potential cases of default and address the concerns raised by lenders. The AA Framework has also started enabling lenders to build effective collection strategies based on a dynamic view of the defaulting borrower’s finances.

A healthy lending environment is desirable not only for the banking industry but also for consumers. A bad credit cycle leads to credit tightening, which impacts the ability of genuine and deserving borrowers to access credit at affordable rates. Given the overarching need to build a healthy credit environment and the initial positive impact of the AA Framework, the regulators and policymakers are supporting its growth. However, there is a need for more concerted efforts to strengthen the framework’s delivery for building a conducive credit underwriting and monitoring environment in the country.

As the AA ecosystem delivers on its potential of furthering credit, Sahamati has taken several initiatives to ensure that the scale-up happens with responsible customer practices. Sahamati has been working towards parameterizing consent templates that define the upper bounds for data usage. At the same time, Sahamati is developing technology infrastructure to support programmatic detection and adherence to the consent templates implemented in the ecosystem, thereby reducing the chances of data misuse. With these robust measures in place, the AA ecosystem is well-placed to fortify the financial sector from fraud & misuse, fostering a safer and more trustworthy financial environment for both institutions and consumers.

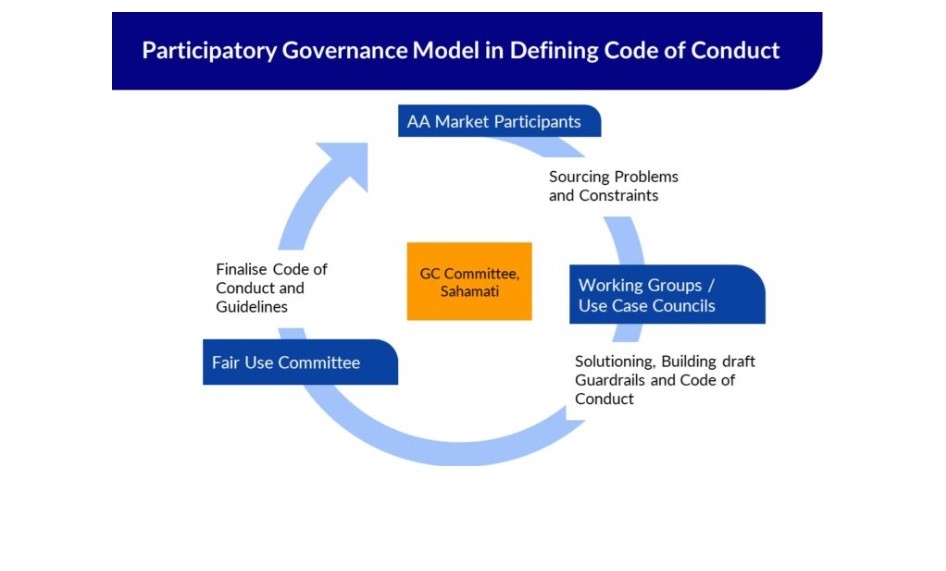

Similarly, the AA ecosystem has strived to formulate ecosystem codes of conduct and best practices through various participatory governance forums comprising diverse participants across sectors, license types, and scales of operations. Recently, RBI released the Omnibus Framework for SRO and is anticipated to come out with sector-specific applications, including a dedicated SRO for the AA Framework, which is expected to strengthen the layer of participatory governance in the AA Ecosystem.

With the right value proposition in place and early impact stories flowing in from early movers, the AA Framework has seen wide adoption and a rapid rise in usage. The AA ecosystem has surpassed 600 active participants across 155 live FIPs, 447 live FIUs, 15 operational AAs, and 60 Sahamati member TSPs, which have facilitated more than 88.88 million consents by June 2024. This growth signals a crucial turning point for rapid adoption and expanded usage. The ecosystem has prioritized establishing robust anti-fraud measures and fair use policies to uphold integrity and trust with scale. These efforts are fundamental in shaping AA’s future trajectory and its impact on the financial sector.

|

|

|

Decommissioning of AA API V1 by REBiT

The Account Aggregator (AA) ecosystem has successfully transitioned to ReBIT API version 2.0.0. Entries in Sahamati’s Central Registry and Token Services were updated in a timely manner to support this migration. We facilitated updating all CR entries in both production and UAT environments, migrating over 600 entity IDs in production and around 500 entries in the UAT environment. This transition to version 2.0.0 signifies a major milestone for the entire AA ecosystem.

|

|

|

|

|

|

|

Sahamati Net:

Strengthening Infrastructure for the AA Ecosystem

Sahamati Net is the technology infrastructure developed and maintained by Sahamati for the AA ecosystem. In the past few months, Sahamati has focused on addressing key challenges such as interoperability, data compliance, data quality, and operational efficiency to improve performance, trust, and reliability in the ecosystem. We have launched the pilot for a Sahamati Proxy that enables ecosystem participants to seamlessly connect with all other entities, eliminating the need for multiple integration points. This initiative aims to streamline both procedural and technical efforts, ensuring a seamless and trustworthy experience for all entities involved in the AA ecosystem. At the same time, we are building Network Observability for the ecosystem, expanding upon the current network monitoring system.

|

|

|

|

|

Launching of Cross-sectoral use case council

The Cross Sectoral Use Case Council has been convened to develop standardized consent templates across all sectors in the financial industry. The council will set guardrails, and establish guidelines to enhance interoperability and customer experience. The Account Aggregator (AA) is the only framework that is cross-sectoral i.e. it enables data transfers among entities regulated by different regulators viz: Reserve Bank of India (RBI), Securities and Exchange Board of India (SEBI), Insurance Regulatory and Development Authority of India (IRDAI), Pension Fund Regulatory and Development Authority (PFRDA), and Department of Revenue (DoR). To address the rise of common use cases across financial sectors, a Cross-Sectoral Use Case Council is needed for establishing consistent goals applicable to all eligible licenses within the AA ecosystem.

|

|

|

|

|

Lending Report: The exponential uptake of AAs in facilitating loan disbursements

Sahamati released a comprehensive report detailing the impact of Account Aggregators on lending in India across various FIU categories such as Banks, NBFCs, and HFCs. This report is the second in the series of lending reports, following the release of the initial report in December 2023. The report discusses in detail on how the AAs have enabled a transformation for the credit providers and enabled greater efficiency and expansion in the lending sector. Click the read more button to access the abridged version of the report. The detailed version of the report is only for the participants of the study.

|

|

|

|

Customer Interaction facilitated by KOSH at Manesar, Haryana

Sahamati had the opportunity to interact with customers of Account Aggregators (AAs) in Manesar, facilitated by Kosh, a new-age Non-Banking Financial Company (NBFC) serving blue-collar workers across Delhi-NCR. This interaction provided us with invaluable insights from various perspectives, including the customers, the lender, and its field executives. We were able to observe firsthand how AAs are making a tangible impact on the lives of blue-collar workers by improving their access to financial services and enhancing their financial well-being.

|

|

|

|

|

Sahamati initiates engaging interactions with the ecosystem to enhance the Consent Templates

Starting in June, Sahamati conducted three open-for-all webinars, “Ask AAnything on Consent Templates and Fair Use System,” with ecosystem members to gather feedback on the consent templates and the fair use system. This initiative has been profoundly helpful in collecting valuable insights, enabling a continuous improvement mechanism for the Consent Templates. These templates were the culmination of collaboration with three FIU councils spread across months. Additionally, the Sahamati team is in discussion with the AAs on the technical implementation of the fair use system, with more information to follow in the upcoming months.

|

|

|

|

|

Sahamati’s recent interaction with Cambridge Judge Business School

Sahamati recently engaged with the second cohort of the COBOF course, hosted by the Cambridge Centre for Alternative Finance (CCAF) at Cambridge Judge Business School. The session highlighted India’s Digital Public Infrastructure (DPI) approach to Open Banking and Open Finance. Participants included policymakers and regulatory representatives from central banks worldwide. The discussion also followed with demonstrations of multiple use cases of AAs that conveyed how the AA framework is setting a strong foundation for a secure digital future.

|

|

|

|

|

|

|

|

|

|

Github

|

|

|

|

|

|

Twitter

|

|

|

|

|

|

LinkedIn

|

|

|

|

|

|

Youtube

|

|

|

|

|

|

|

|

Do not wish to receive mails from Sahamati? Click here to unsubscribe

|

|

|

|

|