| |

|

|

|

|

|

|

|

|

Over the past few months, the AA ecosystem has seen significant strides in strengthening its infrastructure, improving operational efficiency, and implementing Fair Use. The focus for Sahamati has been to enhance the delivery of the framework and increase its usage, trust, and penetration for the 600+ entities that have implemented it. The various impact stories and case studies shared by the leading users have brought out the transformative potential of the AA Framework resulting in higher loans to new-to-credit customers, reduced processing time, nil fraud rates, stronger early warning signals, and improved collections efficiency. Leading banks and NBFCs have increased their efforts to integrate AA across their products and journeys, with a few even opting for AA as the preferred and default option for bank statement sharing.

As part of strengthening the framework, we stepped up our efforts to improve the discovery and data delivery rates, address the data quality issues, build the fair use framework, and work out a long-term solution to deliver efficient interoperability in the AA Ecosystem. Each initiative required close working with the ecosystem participants, regulators, and policymakers via performance reports, bilateral workshops with FIPs/FIUs, building strong technological capabilities, and releasing policy briefs. Results are visible in the usage parameters and overall operational parameters.

Data delivery rates have improved to approximately 60-65% from 35-40% reported a few months back. A few of the ongoing data quality issues have been unblocked. Large banks have started providing transaction narrations and removed limits on the number of transactions per data packet. Additionally, the RBI has clarified the definition of mandatory and optional fields, reducing subjectivity in how banks share profile data through the AA framework. The regulator has also intensified efforts to work with banks to further improve data quality on AA. Sahamati has been conducting bilateral workshops with the Top FIPs to highlight the performance challenges and support them in addressing the critical issues. These systematic improvements will strengthen the AA ecosystem, fostering long-term resilience and enabling sustainable scale-up.

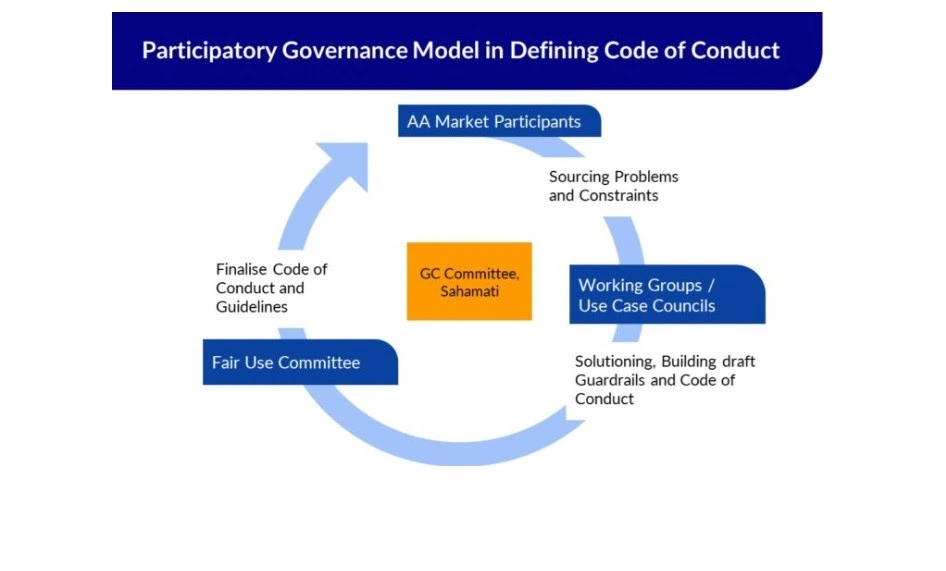

Sahamati has been systematically working on building and implementing governance and best practices in the AA Ecosystem through its fair-use framework. In the latest quarter, the Use Case Council finalized four Fair Use templates, setting clear guidelines for data utilization across sectors. To learn more about AA Fair Use Templates, visit https://sahamati.org.in/aa-fair-use-template-library/. In addition, Sahamati has communicated to the FIUs and AAs about the industry expectations of implementing the fair use framework in a timely manner to ensure an orderly and customer-friendly scale-up.

The expansion of financial information availability on the AA Framework has gained momentum in the past few weeks. The recent ReBIT circular, which calls for activating the Fixed Deposits (FD) and Recurring Deposits (RD) under the new schema, is expected to expand available financial information, benefiting financial institutions. A significant milestone is RBI and REBIT’s initiation of work on activating joint accounts, which will further enhance the usability of AA-based financial data.

On the interoperability front, SahamatiNet Router is ready for a Proof of Concept (PoC) that seeks to develop a router which enables the FIPs, FIUs and AAs to connect router once, doing away with the need for repeated bilateral integrations.

We are approaching the leading FIPs, FIUs and AAs to participate in the POC and would solicit close cooperation and support from the ecosystem to make this initiative successful.

These developments and goals in the AA ecosystem coincide with the broader financial reforms outlined in the Union Budget 2025-26, presented by FM Nirmala Sitharaman, which presents digitisation as the engine for India’s financial sector and economy. By emphasizing credit accessibility, regulatory efficiency, and investment inflows, the budget reinforces the role of digital financial infrastructure in accelerating economic growth. Key measures such as the building of a Grameen Credit Score Framework and the revamped CKYC registry are expected to strengthen the financial sector infrastructure. Likewise, initiatives like the revamped PM Swanidhi scheme and tailored credit cards for micro-enterprises will empower MSMEs and rural borrowers by improving access to credit. These reforms align seamlessly with the AA framework, which enables secure, consent-driven financial data sharing to support more inclusive lending practices.

Furthermore, the role of DPI-Bharat Tradenet in simplifying trade financing, alongside the increase in Kisan Credit Card limits, underscores the growing relevance of AA in digital lending and credit expansion. The decision to raise the income tax rebate limit to ₹12 lakh will further boost disposable income, leading to increased savings and spending power.

Against this backdrop, the strengthening AA ecosystem, coupled with India’s evolving macroeconomic environment, is set to unlock new opportunities for credit access, enhance the design of financial products, and drive sustainable economic growth. Sahamati remains committed to fostering this transformation by ensuring that the AA framework continues to evolve as a key enabler of India’s digital financial future.

|

|

|

|

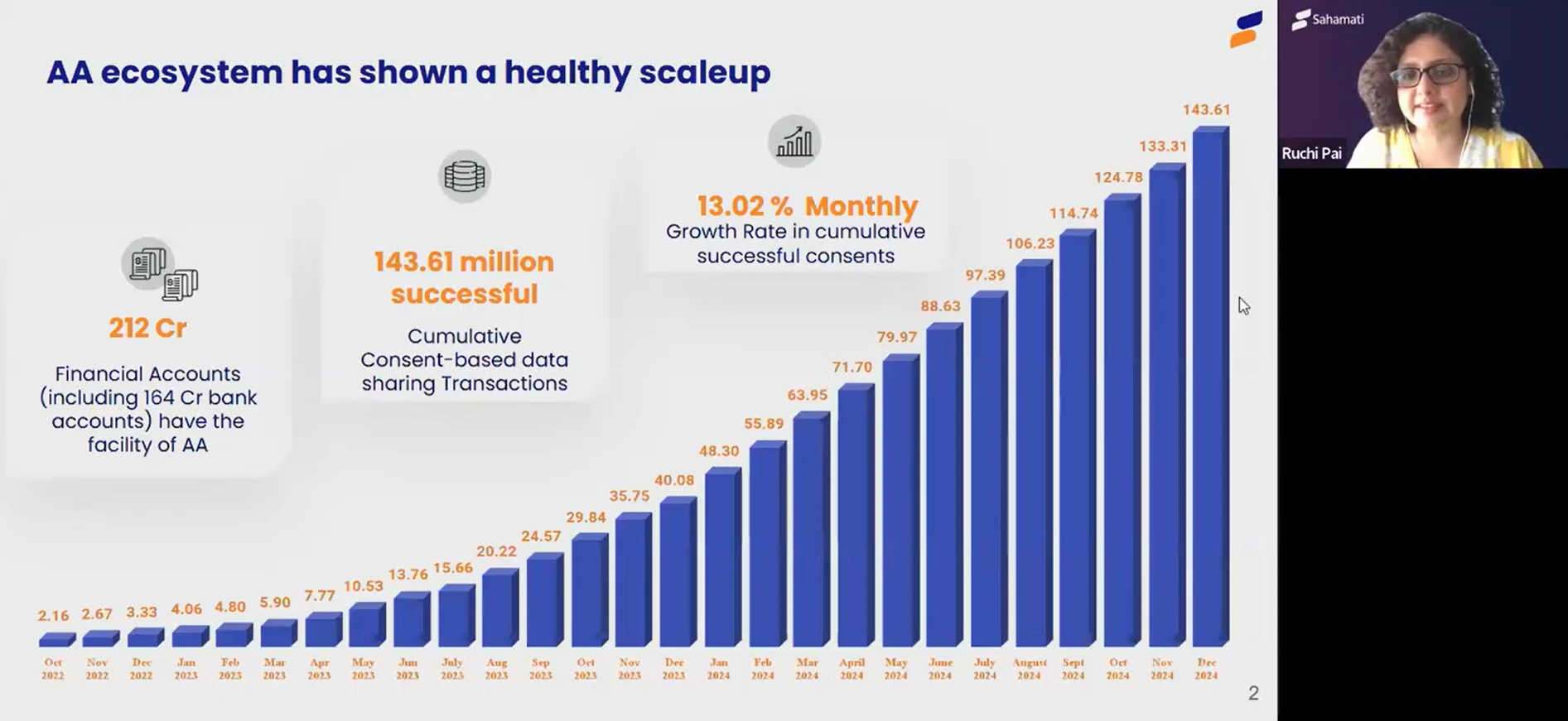

154.06 Million (cumulative) Consent requests fulfilled 128.22 Million (cumulative) Accounts linked on AA 653 REs Live on AA 174 FIPs Live on AA 596 FIUs

Live on AA 89 FIPs

Available on 4 or more AAs

|

|

437 FIs

Sahamati Certification Framework 2,064 UAT Entries in AA Registry 922 Prod

Entries in AA Registry 64,274 (cumulative)

Grievances handled 31,642 (cumulative)

Grievances resolved 323 Dashboards disseminated 12 No. of Fair Use Templates Published |

|

|

|

|

|

|

|

A leading new-age FinTech NBFC has witnessed a transformative impact after integrating the Account Aggregator (AA) ecosystem into its lending processes. By leveraging AA-based bank statement sharing, the company saw a 27% increase in revenue from applications processed through AA, driven by higher credit limits. Additionally, the cost of loan processing dropped by 75%, from ₹400 to just ₹90-100, significantly enhancing operational efficiency. The AA Framework has significantly enhanced trust and transparency, with fraud rates related to bank statements dropping to zero, a factor expected to contribute to lower NPAs. Most notably, 45% of customers successfully completed the AA-based bank statement sharing flow to avail higher credit limits— a sharp rise from the previous 7-10%, highlighting the growing adoption and confidence in AA-enabled lending.

If you wish to learn more about AA, please click here: https://sahamati.org.in/account-aggregators-in-india/

|

|

|

|

Latest in Finance: AA & Beyond

|

|

ReBIT Issues Key Updates on Deposit Schema Changes and Clarification on ‘Mandatory’ and ‘Optional’ Fields in FI Type Schema

ReBIT issued two circulars on January 23, 2025. The first circular announces a major version change (V 2.0.0) for Deposit, Term Deposit (TD), and Recurring Deposit (RD) schemas, with timelines set for July 12, 2025, for operational readiness. Additionally, the circular outlines the process for submitting periodic Adoption Progress Reports and a one-time Adoption Confirmation Report to ReBIT. The second circular provides clarification on the implementation of ‘Mandatory’ and ‘Optional’ fields in the FI Type Schema, encouraging FIPs to provide information for optional fields if available.

|

|

|

|

RBI’s first repo rate cut in 5 years

The RBI’s first repo rate cut in 5 years—25 bps down to 6.25%—is a strong tailwind for India’s credit ecosystem. Easier borrowing will accelerate MSME lending, fuel investments, and spur consumption, especially as income tax cuts are also on the horizon.

|

|

AI in Banking Indian banks are increasingly leveraging AI for regulatory capital planning, liquidity management, and personalized services. However, concerns remain over AI’s “black box” nature, prompting the RBI to introduce oversight mechanisms, including a regulatory sandbox and the Framework for Responsible and Ethical Enablement of AI (FREE-AI). This aims to balance innovation with accountability in financial services.

|

|

|

|

|

|

|

|

The first Pragati Session of 2025, held in collaboration with Finarkein Analytics on January 30, explored the evolving Account Aggregator landscape. The session on “AA 360°: Status, Use Cases, and the Road Ahead,” offered key insights into the ecosystem’s progress in 2024 and the opportunities shaping its future.

|

|

Shalini Gupta, our Chief Policy & Advocacy Officer, joined an engaging panel discussion on ‘Technology and DPI – Transforming MSME Financing’ at the Conference on MSME Financing and the 1st MSME Banking & NBFC Excellence Sammaan – 2025.

|

|

|

|

Product and Technology Updates

|

In the January release, the Product and Engineering team completed all key features required for the Proof of Concept (PoC) milestone. This includes implementing MIS, a subset of Saans powered by Sunbird Obsrv. Enhancements such as code instrumentation for data ingestion from SahamatiNet’s Router and autoscaling capabilities to handle fluctuating traffic loads have been successfully deployed. Critical security measures have also been implemented based on VAPT findings, further strengthening the system’s resilience and performance.

|

|

We are pleased to announce the release of new Fair Use Templates for common use cases that were finalized in Council meetings: a) CT043: Enables regulatory and internal compliance reporting of employee investments, b) CT046: Helps measure the efficacy of government schemes, c) CT010: Facilitates income verification for F&O eligibility, d) CT045: Supports financial condition verification for employees, vendors, and third parties. These templates are designed to enhance transparency and efficiency across various sectors and are expected to be incorporated by FIUs.

|

|

|

|

|

|

Common Myth-Busters

❌ Myth: AA is still in its nascent stage

✅ Reality: The Account Aggregator (AA) ecosystem is experiencing rapid growth, with 600+ FIPs and FIUs now onboarded. The impact is evident, with 154.06 million consent requests successfully fulfilled and 128.22 million accounts linked through AAs, underscoring the increasing adoption and trust in the framework.

❌ Myth: Only limited data is available via AA

✅ Reality: AA enables consent-based access to 16 FI Types, including Deposits (Singly held savings a/cs & sole-prop current a/cs), Term Deposits, Recurring Deposits, Equity Shares (Demat), Exchange Traded Funds, and many more data types.

❌ Myth: AA is only useful for lending

✅ Reality:

Beyond lending, AA powers Wealth management, Budgeting, Expense Management, Insurance, Mutual Funds and Securities, Investment advisory, and Personalized financial services.

|

|

|

|

|

|

|

|

Do not wish to receive mails from Sahamati? Click here to unsubscribe |

|

|

|

|