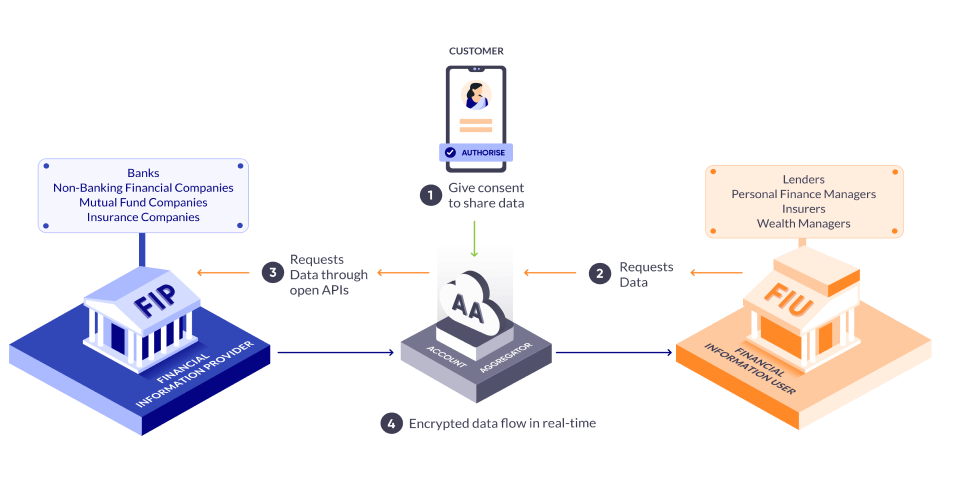

2024 is a critical year for the Account Aggregator (AA) ecosystem in India. The collaborative efforts taken by the industry across law, governance, regulation, technology, and markets are converging. Many crucial developments across these facets have created conditions that enable an exponential scale-up of the AA ecosystem.

Currently, Lending is the largest use case in terms of the percentage of successful consents fulfilled in the AA ecosystem. Digitally-savvy NBFCs, one of the earliest adopters of the AA framework, have benefited from zero fraud rates, higher data collection efficiency, lower underwriting costs, and the ability to monitor loan accounts, leading to the disbursement of Rs. 204 billion across 2.10 million personal and small business loans. In the first half of FY24 alone, the figures are staggering—Rs. 129 billion across 1.35 million loans. The business lending via AAs is set to rise further with GSTN on board.

Followed by lending, the investment and wealth advisory services, predominantly via RIAs, constituted 18% of the consents fulfilled. AAs offer new-age apps with RIA licenses to undertake use cases like spend analyses and personal finance management (PFM) due to seamless access to consumer data.

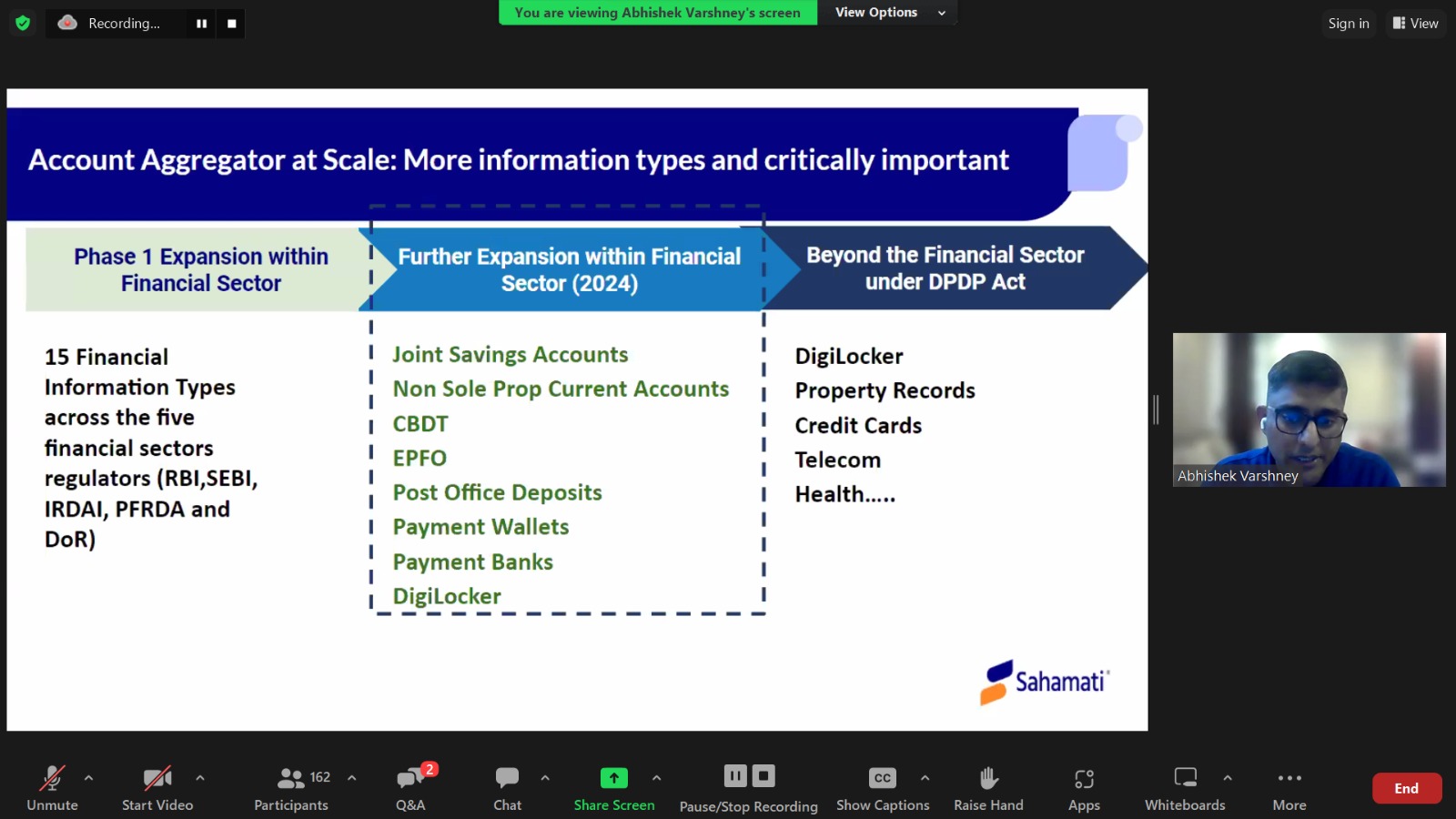

2023 witnessed the AA ecosystem turning truly cross-sectoral. FIPs under SEBI, such as AMCs via the RTAs, and the Depositories and FIPs under IRDAI, such as health insurers, life insurers, and general insurers, went live on the network. Similarly, pension data through CRAs is also live on the network. This has opened up tremendous opportunities for innovative use cases in the ecosystem. In 2024, the usage across public & private sector banks and insurance is poised to increase.

The Reserve Bank of India (RBI) recently released a draft omnibus framework for Self-Regulatory Organizations (SROs) for Regulated Entities (REs) under its jurisdiction. Account Aggregators (AAs) are licensed and regulated by the central bank under its Master Direction NBFC-AA, 2016. The institutionalization of SROs will strengthen governance mechanisms for the AA ecosystem.

The AA ecosystem comprises participants across the four financial sector regulators (FSRs): RBI, SEBI, IRDAI, and PFRDA. The AA framework was initially open to the voluntary adoption of all regulated entities under the FSRs. This year, notifications and consultation papers from regulators have attempted to define the eligible entities joining the ecosystem as FIPs and FIUs. This proactive regulatory stance signals the evolution and maturity of the ecosystem.

Additionally, the AA ecosystem has achieved administrative alignment with the Department of Revenue (DoR) under the Ministry of Finance (MoF) to integrate tax data into the network through strategic entities under their ambit. After the successful joining of GSTN, other strategic entities, such as the Central Board for Direct Taxes (CBDT), Employee Provident Fund Organization (EPFO), etc., have shown momentum to onboard the network.

These developments have created favorable conditions for the significant rise in the adoption and usage of the Account Aggregator framework this year.