|

|

NEWSLETTER · JANUARY 2026 |

|

|

|

We’ve spent three years talking about AA as a ‘promise.’ H1 FY26 AA Impact report data shows it’s now a ‘pipeline.’ With ₹93,420 CR flowing through in half-year, the question is no longer whether it works—it’s who is being left behind as the traditional ‘data moat’ collapses. January 2026 delivered the clearest signal yet: consents climbed by 21.69 million. Data sharing is moving beyond PDFs. Purpose-linked, digitized, and consent-based data access has arrived.

|

|

78%

Rise in daily consents, FY25 vs FY24

| 4–5 Cr

Customers who used a financial service via AA

| 48 hrs

Approvals for MSMEs, down from weeks

| 2.1 Bn

Financial accounts with AA facility — 60%+ of India’s total

|

|

|

The foundation is set, the momentum is visible, and the opportunity ahead is even larger.

|

|

📄New Report Out Now Credit Reimagined: H1 FY26 — The AA Impact Report. We released our Credit Reimagined H1 FY26 report — and honestly, we couldn’t stop at just the PDF. This entire edition is your guided tour through the findings, the numbers, and what they mean for the ecosystem.

| |

|

|

|

I want to start with something we don’t say plainly enough. ₹1.47 lakh crore disbursed across 1.5 crore loans in half-year. One in ten personal loans in India now flows through the AA ecosystem. These numbers didn’t happen because of a mandate. They happened because a group of institutions made a bet on consented, real-time data and found that it worked. The DPDP Rules, notified in November 2025, have given us the legal scaffolding to match, and Sahamati’s Data Privacy Week this January was a reminder that what we’re building isn’t just compliance architecture. It’s a set of values about who owns financial data, and what it should be able to do.

|

|

"The most underreported story in AA is not underwriting. It’s what happens after the loan is disbursed. That’s where the real value of a living data relationship is just beginning to show up." | |

|

The first wave of AA adoption was about replacing the bank statement PDF. That problem is largely solved. The more interesting question is what comes next. The value of AA is being realised beyond underwriting. Lenders are beginning to deploy for risk management through agent monitoring as well as early-warning signals. Leading lenders are catching stress signals before a borrower misses a payment. Large consumer lenders are making AA the default data layer for renewals and top-ups.

The ecosystem’s growth shows clearly in how it uses data. A 22.5% moderation in monthly data pulls, even as consent volumes continued to grow, points to more deliberate and purpose-driven data usage. It’s the ecosystem getting smarter about when and why it fetches data — a direct result of our participatory governance forums that shapes the Fair Use standards. Standards people helped form are standards people actually adhere to. That’s a model worth building on.

|

|

The Pulse: Ecosystem Stats |

|

390+ M

Consents Fulfilled

21+ M

Monthly Consents

177

FIPs Live on AAs

|

|

263+ M

Accounts Linked

10+ M

Monthly Accounts Linked

913 FIUs Live on AAs

|

|

287+ M

Monthly Data Shares

|

960 Live Entities on AA

17 Total Operational AAs

|

|

|

|

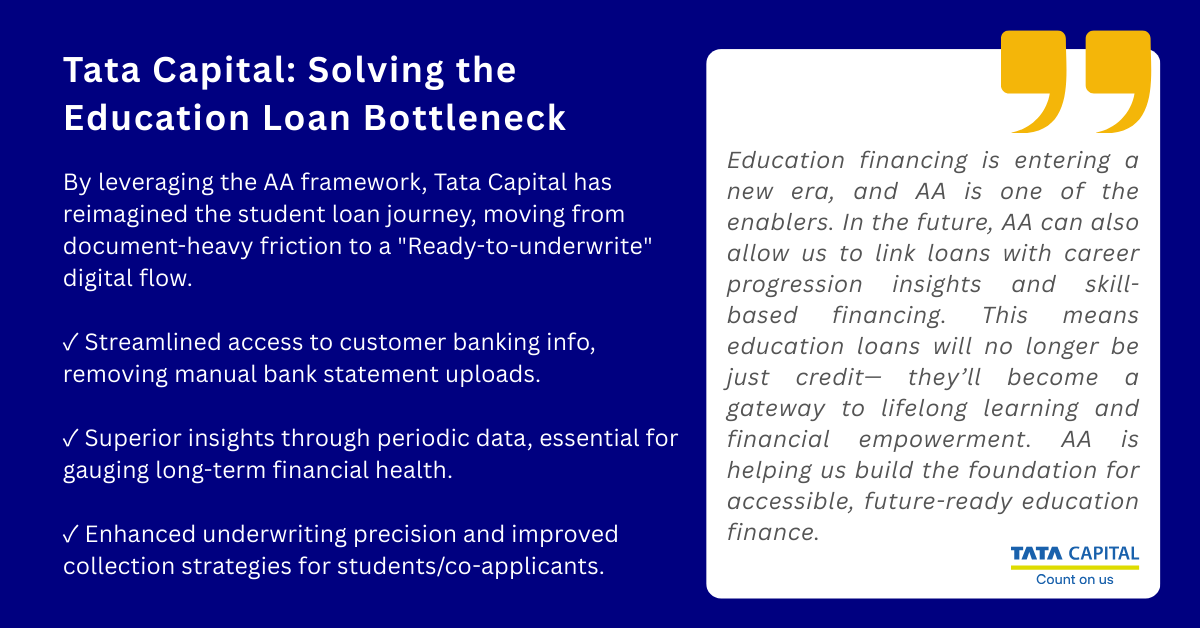

From the Ground: The AA Impact Story |

|

|

|

|

|

|

|

|

|

Which of these is the biggest myth about the AA framework that slows down adoption? |

|

Results published in the February 2026 edition of Varta |

|

|

|

|

|

Sahamati Foundation is a member-driven industry alliance

formed to promote and strengthen the Account Aggregator ecosystem in

India.

|

|

|

|

|

|

|

|

|

|